Blog Post

The European Union and Australia concluded a comprehensive free trade agreement on 24 March 2026. The deal eliminates tariffs on over 99% of EU exports to Australia and removes duties on nearly all Australian goods entering the EU, including critical minerals. Two-way trade between the partners already stands at over €89.2 billion annually (European Commission, March 2026). That number is set to grow significantly.

For supply chain leaders managing sourcing, manufacturing, or distribution that touches either market, the agreement changes the planning landscape in ways that will compound over the next decade.

What the Deal Does: The Numbers That Matter

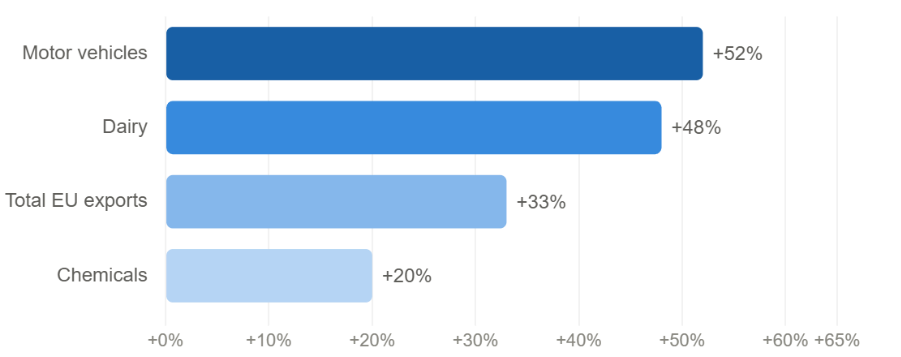

The European Commission projects EU exports to Australia could rise by as much as 33% over the next ten years, with annual export value reaching up to €17.7 billion. European companies will save roughly €1 billion per year in duties from day one. The growth is not evenly distributed: motor vehicles are projected to grow 52%, dairy 48%, and chemicals 20%. For those sectors, tariff removal is either immediate or phased over three years.

| Sector | Projected EU export growth (10 years) |

Source: European Commission press release, 24 March 2026

On the Australian side, almost all exports of manufactured goods and mineral resources (lithium, cobalt, rare earths, aluminum, manganese, nickel, copper, uranium), will enter the EU at zero tariff. EU investment into Australia, already the country’s second-largest source of foreign investment in 2024, is projected to grow by over 87% (Australian Government, DFAT, March 2026).

Agricultural access is the deal’s friction point. Australian beef faces a tariff-rate quota rising to 30,600 metric tons annually over ten years, well below what Australian farming groups sought. The National Farmers’ Federation called the result “subpar,” while European farm groups flagged concerns about competition. For most other agricultural categories, including wheat, barley, dairy, and seafood, terms improve meaningfully.

Five Planning Implications You Should Be Modelling Now

1. Critical minerals sourcing is now a network design question

For any European manufacturer using lithium, cobalt, rare earths, or aluminum (which covers EV production, battery manufacturing, aerospace, defense, and industrial automation), the FTA creates a structurally more stable and now cheaper sourcing lane from Australia. Import duties that previously tilted the economics toward Chinese suppliers are eliminated.

This is a network design decision, not just a procurement one. The transit lane from Western Australia’s mining regions to European manufacturing clusters runs approximately 17,000 km, with sea transit times of around 20 to 25 days on bulk carriers. That means longer supply lead times, higher safety stock requirements, and different inventory positioning than Chinese-origin supply. Planners need to model the full landed cost — tariff savings plus transit costs plus inventory investment — not just the headline duty rate.

The question to run now: What does the end-to-end cost and risk profile of Australia-origin critical mineral supply look like versus China-origin, under the new tariff structure? Build that scenario before your next sourcing contract renewal.

2. EU export growth into Australia creates new distribution requirements

A 33% projected growth in EU exports over the next decade means the Australian market moves from a tail market to a planning priority for many European manufacturers and consumer goods companies. Transit times from major EU logistics hubs to Australian ports run 20 to 28 days depending on origin. Service levels standard in European distribution cannot be maintained by European DCs alone.

Companies planning for Australian market growth face a clear choice: local inventory positioning, a regional Asia-Pacific hub such as Singapore, or a service level agreement that honestly reflects the distance. The companies that build distribution infrastructure before tariff-driven demand materializes will have an advantage over those that scramble later.

The question to run now: If your Australian volumes grow 20% over the next three years, can your current distribution setup absorb it, and at what service level and cost?

3. Agricultural quota dynamics require careful modelling

For agricultural supply chain planners, the FTA is more complex than a simple tariff cut. The quota structure, where duty-free access applies only up to specified volume thresholds, creates a planning variable that changes the effective cost of supply depending on whether annual volumes sit above or below quota. This threshold needs to be modeled explicitly, not averaged. For sellers into the Australian market, the geographical indications protection list also has compliance implications: Australia has agreed to protect 165 EU GIs for agri-food products and 231 GIs for spirits. Any product sold under a name that is now a protected EU GI requires a compliance review with a real timeline.

4. Investment flows will reshape production footprints

EU investment into Australia is projected to grow by over 87%. At that scale, the impact is not portfolio reallocation. It means European manufacturers building or acquiring processing capacity in Australia, particularly in minerals and clean energy. If the economics of Australian mineral processing improve as EU capital flows in and tariff costs flow out, the optimal location for intermediate processing in a European supply chain may shift. This is a 3–5-year planning horizon, but the supply agreements and investment decisions that define it are being written now.

5. The Australia-EU corridor is now a strategic lane

For most European supply chain teams, Australia sits at the edge of the geographic model, managed as a tail market. The FTA changes that classification. Combined with Australia’s role in critical minerals and the EU’s accelerating Indo-Pacific trade strategy, the Australia-to-Europe corridor now warrants strategic-level planning: appropriate safety stock, route redundancy, and established carrier relationships.

The Practical Checklist

If you use critical minerals in manufacturing: Run a full landed cost comparison for Australia-origin versus China-origin supply under the new tariff structure, including transit time and safety stock impacts.

If you export EU goods into Australia: Model a demand scenario for 15 to 25% volume growth over three years. Identify the distribution infrastructure gap and whether your current 3PL relationships can absorb it.

If you operate agricultural supply chains: Map your exposure to the quota thresholds on both sides and check any branded products against the EU geographical indications protection list.

If you lead supply chain strategy: Scenario-plan the impact of significantly increased EU investment in Australian minerals processing on your current supplier base and intermediate processing locations.

How can AIMMS help?

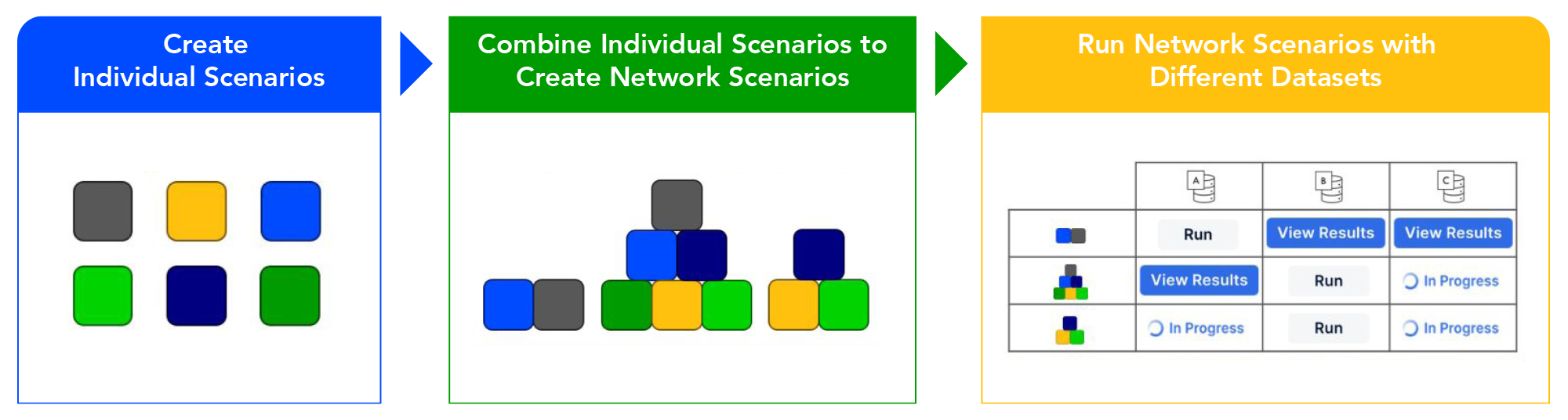

The EU-Australia FTA creates decisions that play out across three time horizons simultaneously: the long-term network structure, the medium-term operational flex, and the immediate routing and fleet question. AIMMS SC Navigator, Transport Navigator, and the Tactical Planning module are built to address exactly that stack.

SC Navigator answers the strategic question: where should Australian minerals sit in your sourcing network, and what does the full landed cost look like once you account for the new zero-tariff structure, 20 to 25 days of sea transit, and the safety stock that distance demands? It models cost, service level, risk, and CO2 simultaneously across scenarios — Short Growth, Extended Growth, and Structural Redesign — giving leadership a decision-ready comparison rather than a single-point recommendation.

Transport Navigator makes the strategy executable. Once your preferred network scenario is chosen, it designs the routes, sizes the fleet, and builds the delivery schedules — validating that the plan works operationally before you commit. A strategy that optimizes well in a network model is only valuable if it can actually be run. Transport Navigator is the step that confirms it.

The Tactical Planning module manages the in-between. As tariff phase-outs, investment deployment, and demand build unfold month by month over the next 3 to 24 months, it lets you flex the network — adjusting inventory positioning, activating secondary suppliers, managing quota thresholds — without rebuilding the full model every time conditions shift. Most supply chain teams either plan strategically or react operationally. The Tactical Planning module is what closes that gap.

The planning teams that act now, while the window is open and before the new cost structure shows up in their actuals, will be the ones with the network in place when the opportunity fully arrives. .